Scale Step by Step

Or why you can only grow a startup on a solid foundation

The Next Founder helps founders build great startups. We offer advice on managing your mental health and productivity, hiring and managing great people, building a strong culture, and keeping people aligned and working on the right things. See the series overview at Welcome to The Next Founder and find out more about me at My Story.

"The best startups don’t rush to grow; they perfect their foundation so they can sustain growth."

— Reid Hoffman

"The hard thing isn’t setting a big, hairy, audacious goal. The hard thing is laying brick after brick, day after day."

— Ben Horowitz

"Don’t worry about scaling. Worry about building something worth scaling."

— Paul Graham

Running in sand wearing ski boots

On Saturday morning, you wrap yourself in a bathrobe and brew tea to regroup after a frantic week. You ask your AI assistant Aimee to extract to-dos from transcripts of the week’s meetings. Aimee spits out a task salad that makes you wonder if your little LLM friend is hallucinating.

On Tuesday, your Director of Sales blew up when you asked her why the forecast is so meager. In a millisecond, she deflected the blame to your marketing team, claiming they are delivering unclosable leads from prospects who stretch the definition of “qualified.”

The next day you asked your Director of Marketing why the leads are weak. He says that since you don’t have any happy customers, he has no idea what value propositions resonate with buyers. You brought your Director of Customer Success into the meeting, who says, “I can’t convince customers to love a product that is trying to solve so many problems that it doesn’t solve any of them well.”

You finished the week going out for drinks with your CTO / co-founder. You hoped to confide, commiserate, and brainstorm solutions, but instead, he explodes, “You are so obsessed with closing deals before the Series A, you stopped listening. We are trying to sell to too many different types of customers who need different things. I told you that it’s too early to hire a sales and marketing team, and soon we’ll be laying people off. I’m not sure how long I can last since this is not what I signed up for!”

You are left reeling, wondering how your “high growth” startup got stuck in the mud. But you aren’t the first startup struggling with growth, and you might be able to recover if you Scale Step by Step.

Too fast, too slow, or just right?

As we covered in Embrace Contradiction, founding a startup forces you to balance seemingly contradictory ideas, many of which involve how fast to grow.

A startup exists to grow. Grow is what a startup does. The best startups grow 3-10x per year, and a startup that doesn’t grow will die. Great founders are willing to leave their comfort zone, take risks, and invest resources to achieve that growth.

But that pressure to grow can lead to a common startup failure path: scaling prematurely. Those founders try to speedrun scaling by copying the tactics of high-growth startups, like hiring a marketing team to build a pipeline, sales reps to close deals, and cramming the product full of features. They build a startup that is like the 10-year-old neighbor kid missing free throws in the driveway despite wearing his new Steph Curry jersey and Curry Series 7’s.

So how do you know when it’s time to grow, and how do you know when you need to lay more of the foundation needed for growth?

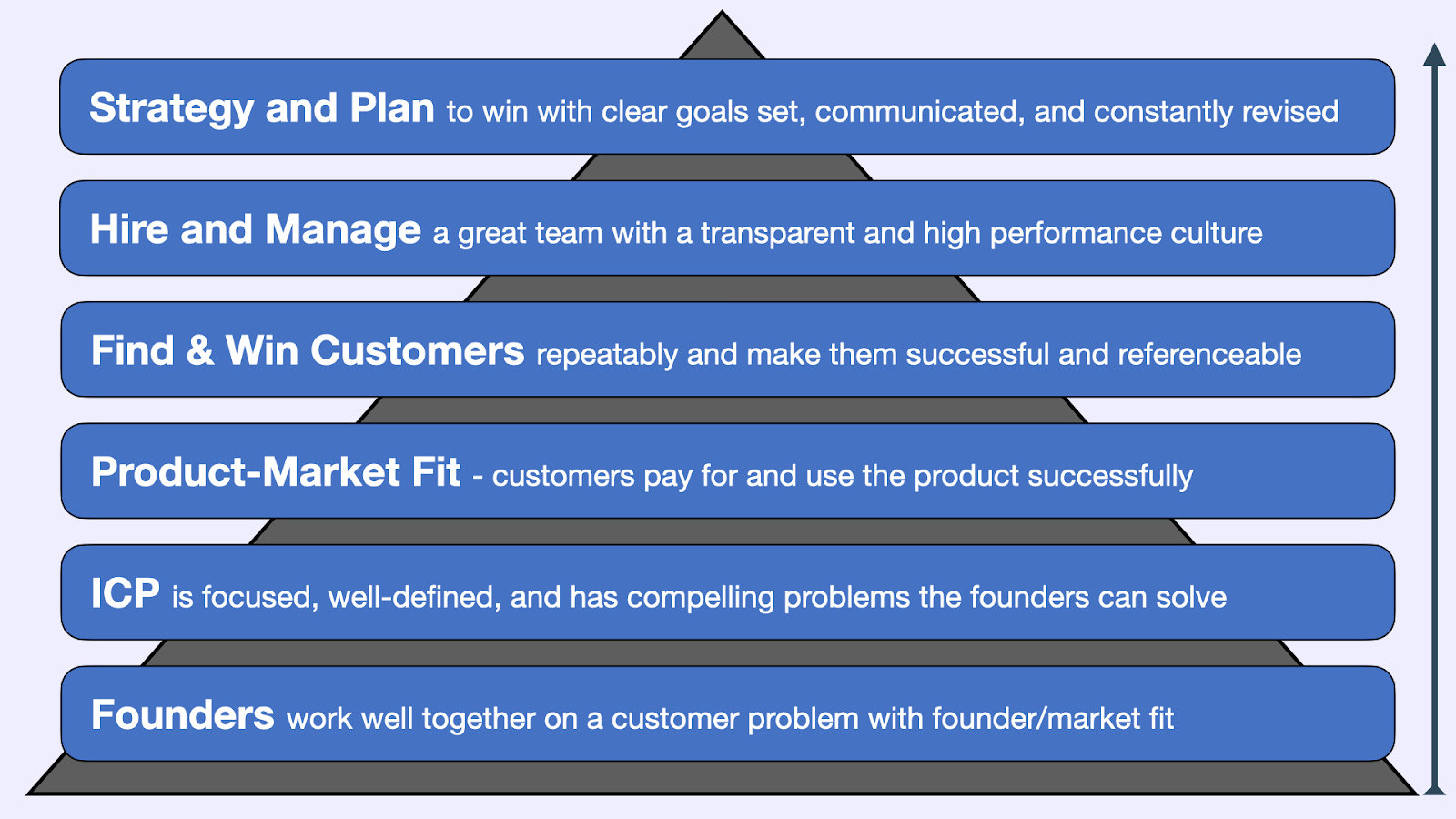

The Startup Scale Hierarchy

You can think of startup growth as a hierarchy, where each level serves as the foundation for higher level1. Trying to climb too quickly up the hierarchy can cause the whole thing to topple down, but moving too slowly can cause you to lose the market to competitors.

Each level is a vast topic that we can’t do justice to here. Most startup advice, including from Next Founder, applies to one of these levels. We’ll limit our discussion to some of the signs that each level is solid enough to start supporting investments at the next level.

Level 1 - Founders work well together with founder-market fit

At an early-stage startup, the founders are the company. They decide which customers to focus on, what problems to solve, and design and build the product. They hire and manage the team and set the culture.

The founders in our vignette were disconnected from each other and were losing faith in their business. You can avoid that if you:

Invest in your co-founder relationship

More than half of startups fail due to problems with the founding team, often leading to a founder break-up2. The founders might discover they aren’t equally committed once they discover how hard a startup is. They might find they have different working styles or that they flat-out don’t like each other. In Start Out the Right Way, we talked about a few ways you can discover if you and your co-founder are a good fit and set the right expectations at the start.

Find a problem where you have “founder-market fit”

No founder is universally talented: their knowledge, passion, and skills are only relevant in the context of a building a specific startup to win a specific market. The founders must either arrive with a deep understanding of their market or quickly develop that understanding. Plan to spend a great deal of time with your customers to get to know them, understand their problems, and ensure that you are the right team to solve them.

Avoid burnout

It usually takes ten years or more to build a sizable startup, so you are going to spend the greater part of a decade working with your customers on their problems. As we discussed in Train Like a Startup Athlete, investing in your physical, mental, and emotional health enables you to work hard over a long period.

A great founding team isn’t enough, though. You need something worth working on, meaning:

Level 2 - A focused and well-defined ICP with an urgent problem

A great startup needs a great market, meaning a customer with a problem you can solve. That combination of customer and problem doesn’t just drive what product to build. It also drives your pricing, business model, and average deal size, which in turn drives the go-to-market strategy, what metrics to track, and even who to hire.

The founders from our vignette built a company where no one knew who the customer was or what they needed, so the team was running in circles. To avoid that, make sure you:

Find a problem that customers need solved urgently

The most common startup failure path is simply not finding a customer problem so critical that customers will buy a solution from a startup to solve it. Ask hard questions about whether what you are working on matters, work with prospects to incorporate their feedback, and experiment and pivot until you find something that resonates.

Pick a focused Ideal Customer Profile

In Spread the Good Word, we talked about how most startups struggle to get anyone to pay attention to them at all. After all that rejection, you’ll be tempted to say “yes” to anyone who picks up the phone. But if those customers are too different from each other, your startup can find itself with a mishmash of customers from different industries with different problems, none of whom are happy. Focus on a well-defined ICP that feels the most urgency to solve the problem, even if you need to say “no” to other prospects along the way. You can expand your ICP over time, but it’s almost always better to be very focused at the start.

Know your positioning

Most founders know and love their product and assume everyone else will, but prospects have an odd way of refusing to go along for the ride. When a prospect considers your product, they’ll mentally “position”3 it by considering what problems it solves, how urgent those problems are, and what the alternatives are. Your startup’s positioning then drives how you sell and who you compete with. In some cases, you can turn your product from a “nice to have” to a “must have” simply by reframing who you are for and why they should care about you.

Of course, you have to actually to solve that problem, which takes us to:

Level 3 - Product-market fit

Your product has to solve the customer problem well enough for customers to use it, choose it over the competition, pay for it, and recommend it. Yes, we are talking about Product-Market Fit4. PMF is such an important step that startups are often described as either “pre-product market fit” or “post-product-market fit” since they have such different challenges. Many first-time founders are shocked to learn how difficult and rare it is for a startup to find PMF.

You know you’re converging on product-market fit once you:

Obsess about a customer problem

This is worth repeating since it is probably the primary source of startup failure. At most startups, the founders have the skills they need to build the product, so when customers are apathetic, it’s because you haven’t solved a problem they are losing sleep over. Don’t just ask yourself how well-designed, fast, and feature-rich your product is; validate if your customers care about the problem you solve in the first place.

Ship a product that solves that problem

Of course, you have to build a product that works, is a joy to use, and spits out metrics that prove you have solved the customer problem. This rarely happens right away, so you need to get the product in front of customers in your ICP and keep testing and iterating until you have a handful of customers who love it. Plan for this to be iterative, where you need to experiment with different ICPs, value propositions, and features to get it all to line up.

Find customers who love you

The first baby step towards product-market fit is to find a handful of customers who use your product, love it, and are willing to pay. Most founders will tell you that getting those first few customers was agonizingly slow and required them to do “things that don’t scale”5 like working their personal network, camping out in their prospects’ office, and offering generous discounts. Do whatever it takes to acquire and retain those customers and turn them into evangelists. Don’t worry about how you will get 1000 customers until you’ve gotten ten.

But you can’t stay at ten forever, which means you need:

Level 4 - Scalable and repeatable way to find and win customers

Product-market fit with a handful of customers is a prerequisite to scaling, but it doesn’t guarantee anything. You only succeed if you use that early traction as a springboard to find scalable ways to build your business.

The startup from our vignette was flailing since the team had no idea how to find and win customers. You can flail less if you:

Train your team to close deals

The founders drive the first sales at a startup by building relationships with early users, ensuring the product meets their needs, and converting them to paid customers. You only scale from there once other team members can do the same thing. Although you should always stay involved in sales, invest in figuring out what messages and value propositions resonate with your buyers, and train and support your team to close deals with minimal help from you.

Learn to build pipeline

Your first few customers might come from your immediate network, including former coworkers, friends, relatives, classmates, or peer companies in your incubator program. But no matter how connected you are, your network will run dry pretty soon. You and your team need to learn where prospects in your ICP hang out, find ways to reach them, and learn what messages and value propositions resonate enough to get them into your pipeline.

Expand with discipline

Founders always feel both internal and external pressure to grow, so they can be tempted to prematurely expand their ICP and chase prospects who won’t be successful. Like the founders in our vignette, they feel pressure to add sales and marketing staff to chase growth, reasoning, “you need to spend money to make money,” only to find they are spending without making. Be deliberate about which investments to make and when, and don’t expect that adding people will magically bring in new business.

At this point, you are getting smarter about your customers and how to build a business that solves their problem, but now you need someone to do the work, which takes us to:

Level 5 - Hire and manage a great team

Almost any founder scaling a startup will tell you that most of their problems involve finding great people, keeping them, and getting them to work well together. Although AI is helping startups grow with smaller teams, the smaller the team, the more critical each role is.

You’ll know you’re on track to building and managing a great team once you can consistently:

Bring in the right people

Recruiting is time-consuming. Adding a single person to the team can take dozens of hours of sourcing, interviews, reference checks, and courting the candidate. Most startup teams spend so much time building their product and finding customers that they can’t imagine finding extra hours to recruit their team. You have to find a way to do it, even if you have to drop some other tasks. Adding the right people to your teams gives you way more back than it costs. In Find Your People, we discussed what kind of people to target.

Move out the wrong people

No matter how well you hire, you will always make some mistakes, where you hire someone who just isn’t working out. You’ll also find that as you grow, people who were great in the early days are not scaling as your company scales. When you recognize that someone is not working out, move quickly to help the person improve, find them a new role, or ask them to leave. The best founders are uncannily good at this.

Learn how to delegate

Many startup management dilemmas involve what to delegate and how. You won’t scale if you make yourself a bottleneck, but delegating the wrong work to the wrong people can slow you down even more. In Activate Founder Mode, we discussed how to know the difference.

Build an open and transparent culture

Any founder will tell you that they prefer working for an innovative startup than for a large, sluggish incumbent, but ironically, many founders build BigCo cultures at their startup anyway. They are reluctant to share information with their team or trust them with decisions, as we discussed in Know Your X's and Y's.

But the best team in the world doesn’t help you unless you ask them to work on the right things, which means:

Level 6 - Plan and execute a strategy to win

Startups always live in a world of scarcity, where they can only afford to prioritize a few goals at a time. You need a strategy that tells you which of those goals to prioritize based on a strategy to win your market. You then need to track those goals, make sure each team member knows their role in accomplishing the goals, and replan regularly.

To excel here, you need to:

Have a clear strategy to win

Every successful startup attracts competitors, and in most markets, only the top handful of competitors capture the bulk of the value. You need a strategy and plan to become one of them. That strategy has to represent clear choices and tradeoffs, such as which ICP to focus on, how to expand that ICP, how to win customers, how much risk to take, and what product and distribution strategies to invest in.

Plan and replan regularly

All startups compete in dynamic markets, so they gain insights into how to win their market daily. Your job isn’t to set a long-term plan and then white-knuckle it against all opposition. Your job is to stay in learning mode and constantly update your plan as you learn. But startups also need some continuity, where they don’t fall victim to “shiny object syndrome” and chase every new opportune that comes along. Assume you will plan and replan often, but be thoughtful about the changes you make and take time to explain them to your team.

Manage the company based on the plan

A plan isn’t just a quarterly corporate exercise, where you write some goals down, show them to the board, then put them into a virtual drawer until the next quarter. A well-run startup reviews the plan daily, asks how they are tracking the plan, and changes the plan based on new information. You’ll know you’re on track when you use your plan daily to make decisions and facilitate conversations with your team.

Using the Startup Scale Hierarchy

The hierarchy doesn’t give you a roadmap or a checklist that guarantees you’ll build a great startup, but it does give you a framework to guide certain decisions. You can refer to it when you:

Don’t skip steps

Every startup, especially venture-funded ones, feels enormous pressure to grow. You’ll feel a lot of pressure to skip steps, but that can lead to several problems:

Pivoting into a market where the founders don’t have a lot of knowledge or conviction.

Building a product without a comprehensive understanding of your ICP and their challenges.

Hiring sales and marketing staff before reaching product/market fit.aa

LARPing a successful startup by “playing house”6 and leasing a nice office, hiring a Head of Finance, launching a podcast, and doing the things that successful startups do without actually being one.

But don’t move too slowly

But, this hierarchy is not linear, where you master each level before leveling up. Sometimes you’ll have to work on several levels in parallel. For example, finding product-market fit requires experimenting with different customers, problems, and features until you get them all to align. And sometimes, you’ll need to poke your head up a level and start investing before the previous level is completely baked, for example, hiring and onboarding a couple of sales reps (a multi-month process) before you have converged on your sales playbook. Only you can decide what level of risk you are willing to take, based on how much funding you’ve raised, how quickly your market is moving, and if you are willing to make hard choices when things don’t work (like laying off those same sales reps once you realize you hired them too soon!)

Better understand investors

The hierarchy helps you understand investors since different investors invest at different levels. Although every investor needs to believe you will eventually master every level, they vary based on the amount of progress and proof they need.

Angel and pre-seed investors invest at the bottom of the hierarchy, mainly focusing on the founding team and the problem they are tackling.

Seed and Series A investors want more evidence of product-market fit and that you have found a scalable GTM motion.

Later-stage investors want to see a fleshed-out executive team, compelling metrics, and a long-term plan to win your market and build competitive advantage.

Always target investors who invest at your level, center your pitch around evidence you’ve mastered those levels, and give a preview of how you plan to master subsequent levels, for example how you plan to build barriers to entry.

Stay vigilant

No matter how high you climb in Maslow’s Hierarchy, you never stop needing food and shelter. This hierarchy works the same way. You have to keep investing in your co-founder relationship as new challenges arise. You have to invest in burnout avoidance, which can get harder every year. You can’t take product-market fit for granted - you can lose it over time. You can never stop getting better at winning customers since new competitors always pop up. Monitor your metrics and momentum at every level, and never get complacent.

Be ambitious and take risks when growing your startup, but always ask if your foundation is strong enough to support that growth. Good luck!

If you have feedback or suggestions for future posts, please comment or contact us at michael@nextfounder.co.

Yes, this might look familiar if you know about Maslow’s Hierarchy of Needs. Many thanks to Abraham Maslow. I’d offer him advisory board share if he were still with us.

Noam Wasserman’s The Founder’s Dilemmas is the classic source on the difficult decisions founders need to make about what they want out of their startup.

April Dunford’s Positioning blog and book are great sources for all things startup positioning.

See A16Z’s 12 Things About Product-Market Fit and Marc Andreessen’s The Only Thing That Matters.

I realize that I refer to Paul Graham’s Do Things That Don’t Scale in every other post, but there is a reason for that.

Paul Graham (again) was the first to write about startup founders “Playing House.”

Brilliant, as always